Hi. My name is Erin, and I hate my mortgage.

I hate it. It is my last debt. I’ve paid off student loans, personal loans, credit cards, HELOCs, and car payments. Now I’m down to the mortgage. And I want that sucker gone as soon as humanly possible.

I bought this house in June of 2019 and took a 15-year mortgage that I pay bi-weekly. Fortunately, due to the sale of my previous home, I had a sizable down payment.

I considered taking a 10-year loan, but the 15-year loan gives me a little more breathing room in case I ever need it, and there wasn’t much difference between the loans, especially if I’m aggressively hitting the balance with extra payments.

Before making an offer on the house, I sat down one night and ran numbers. How quickly could I pay this off? I found this super helpful spreadsheet (I’m using the bi-weekly one on that page) that helped me figure out that I could probably pay it off in 6 years—and that’s what I’m aiming for.

If you’re right there with me in wanting to pay off that mortgage once and for all, let me show you how I set it up in YNAB to supercharge my progress.

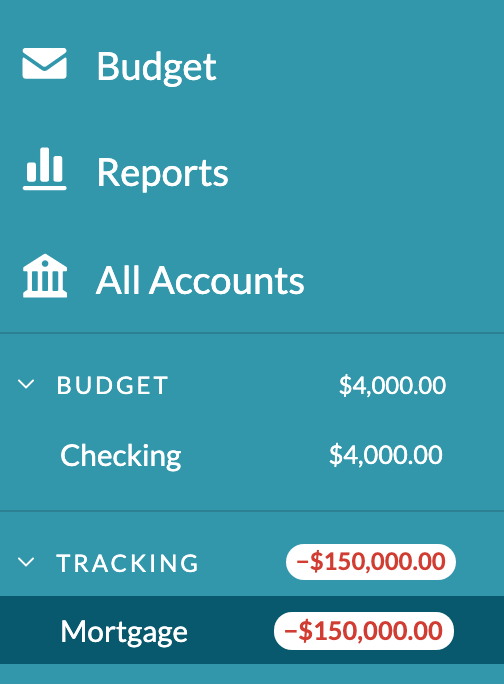

I Set Up My Mortgage as a Tracking Account

I set up my mortgage as a tracking account.

Before I walk you through the nitty gritty of how I manage that, I want you to know, you do NOT need to add a tracking account. The most important thing you can do is budget for the payment and then make the payment. That is the simplest approach and the only necessary part.

For my last house, I did not track the mortgage. It was a big number and I knew it was going to be a while, so I didn’t set it up as a tracking account and just paid the monthly line item in my budget.

But for this one, I want to see that balance so I can watch it go down. I’m attacking this debt, and awareness helps me here.

First, I added a tracking account with the balance of my mortgage. Make sure you choose Tracking > Liability as the account type.

The balance of a tracking account sits outside the budget. That $150,000 I owe? It has zero impact on the budget, but I can see it in the sidebar on the left and also in my net worth report.

“Alrighty” you say, “but how do I know that balance doesn’t affect the budget?”

The thing that connects an account to the budget is the category column. You’re either categorizing income as To be budgeted to send it to the budget, or you’re categorizing to the category you spent from to remove money from the budget.

There’s no category column in a tracking account.

It’s simply not connected to the budget at all.

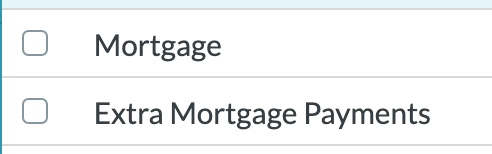

I Have Two Categories for the Mortgage in My Budget

I separate them out by my normal monthly mortgage payment, and then I have a category for any additional money to put toward extra payments on my mortgage. When I budget toward the extra mortgage payment category, I like that I’m making a very clear and deliberate decision.

You don’t have to separate them out, you could just budget extra to the mortgage category (but I find it’s cleaner to do it this way). Because my mortgage is biweekly, there are two months a year where the mortgage payment is higher. I use the main mortgage category to make sure I’m preparing enough for the payment I have to make. I don’t want to mess that up.

When a Payment is Made

When I make a payment on my mortgage, there is a line item in my budget that shows a categorized transfer to my mortgage account.

Why categorized? Money is leaving my budget. Why a transfer? So it will be recorded in the mortgage account.

If I make a regular payment, it looks like this:

Notice the balance on the mortgage account was also updated.

It’s the same process if I make an extra payment, I just choose that Extra Mortgage Payments category instead.

Notice again, the account balance has been updated. And if we look at the budget, we can see the outflows in those categories.

How I Account for Mortgage Interest

So, we’ve accounted for payments to the mortgage. But remember, they are charging me interest on this loan. Payments make the balance go down, but interest makes it go up.

I have to account for that in order to keep the account balance correct. I’m a simple girl and like to keep things simple, so once a month I reconcile the mortgage account. It won’t be right because of the interest, so I just let YNAB do the math and make an adjustment.

Here’s what that looks like:

So there you have it! That’s how I do my mortgage in YNAB and hopefully no later than December of 2025 it’ll be gone for good.

Want to learn more YNAB tips and tricks? Sign up for our weekly newsletter to stay in the loop!

The post How to Do Your Mortgage in YNAB appeared first on You Need A Budget.

Via Finance http://www.rssmix.com/

No comments:

Post a Comment