So, you’ve chosen to share your life, your space, your self, your bed, your innermost hopes, fears, successes, and failures—but you put your foot down at sharing a bank account.

Hey, some things are sacred, right?

Although a wise man once said, “When it comes to budgeting with a partner we take a hard line: If you’ve joined your lives, you should join your finances. Joint accounts all the way,” a truly wise man (or woman) understands that life is not a one-size-fits-all situation.

(We’re the wise human in both of these scenarios. Let us have this one, okay?)

If keeping the peace in your household involves maintaining separate accounts, you’ll get no judgment from us. We’ll leave that up to the disapproving family members who are all up in your business. Every family has one.

We’re here to help. And to work in sly references about our wisdom.

Let’s take a look at how you can make budgeting for couples work without combining your checking, savings, or investment accounts.

Budgeting for Couples With Separate Accounts

To make this easier to follow, let’s take a peek at how an imaginary couple, Jamie and Jordan, manage their individual and shared finances.

First, the basics. For this method, they use the following:

- Jamie’s personal savings and checking accounts

- Jordan’s personal savings and checking accounts

- Shared savings and checking accounts for the household

- They’ve got three budgets set up in YNAB: Jamie’s, Jordan’s and one for the household (they’ve tried all the budgeting apps and they like the convenience and visibility of YNAB to stay on track for long-term financial goals).

Yes, their financial plan comes to a total of three budgets and six accounts, not including investments. (You can see why joint-everything would be simpler, eh? Just an observation, not a judgment!). So how can they manage their household budget successfully? We’ll explain.

1. Budget Your Paychecks Separately

When Jamie gets an inflow of new dollars, they’ll be assigned in Jamie’s YNAB budget. Likewise, when Jordan gets an inflow of new dollars, they’ll be assigned in Jordan’s YNAB budget. This gives Jamie and Jordan complete control over how to assign their own dollars and should, theoretically, lead to fewer disputes about spending.

When Jamie was creating a budget, she only added categories and accounts specific to her. Same goes for Jordan’s budget: it only had Jordan’s categories and accounts. These are things like their own discretionary food or coffee budgets, their own fun money, perhaps gas money, and any bills they’re solely responsible for.

2. Contribute to a Shared Account for Household Expenses

There’s one caveat to this approach: every payday, Jamie and Jordan both agreed to contribute a predetermined, set amount to the shared household checking and savings accounts. This pays for shared expenses and helps them meet their joint savings goals.

Here’s how they track this:

- Jamie and Jordan each have a category in their individual budgets called Shared Budget (or maybe something snazzier than that, depending on their creativity level).

- They contribute a set amount to this category each month.

- This money gets transferred to the budget they share. (Categorize the outflow as a transaction under Shared Budget and then add that amount as an inflow under “Ready to Assign” in the budget that they share.)

In the case of Jamie and Jordan, their contributions are equal. If one partner makes significantly more than the other, it might make more sense to contribute based on a percentage of income. This is the stuff you’ll need to work out together.

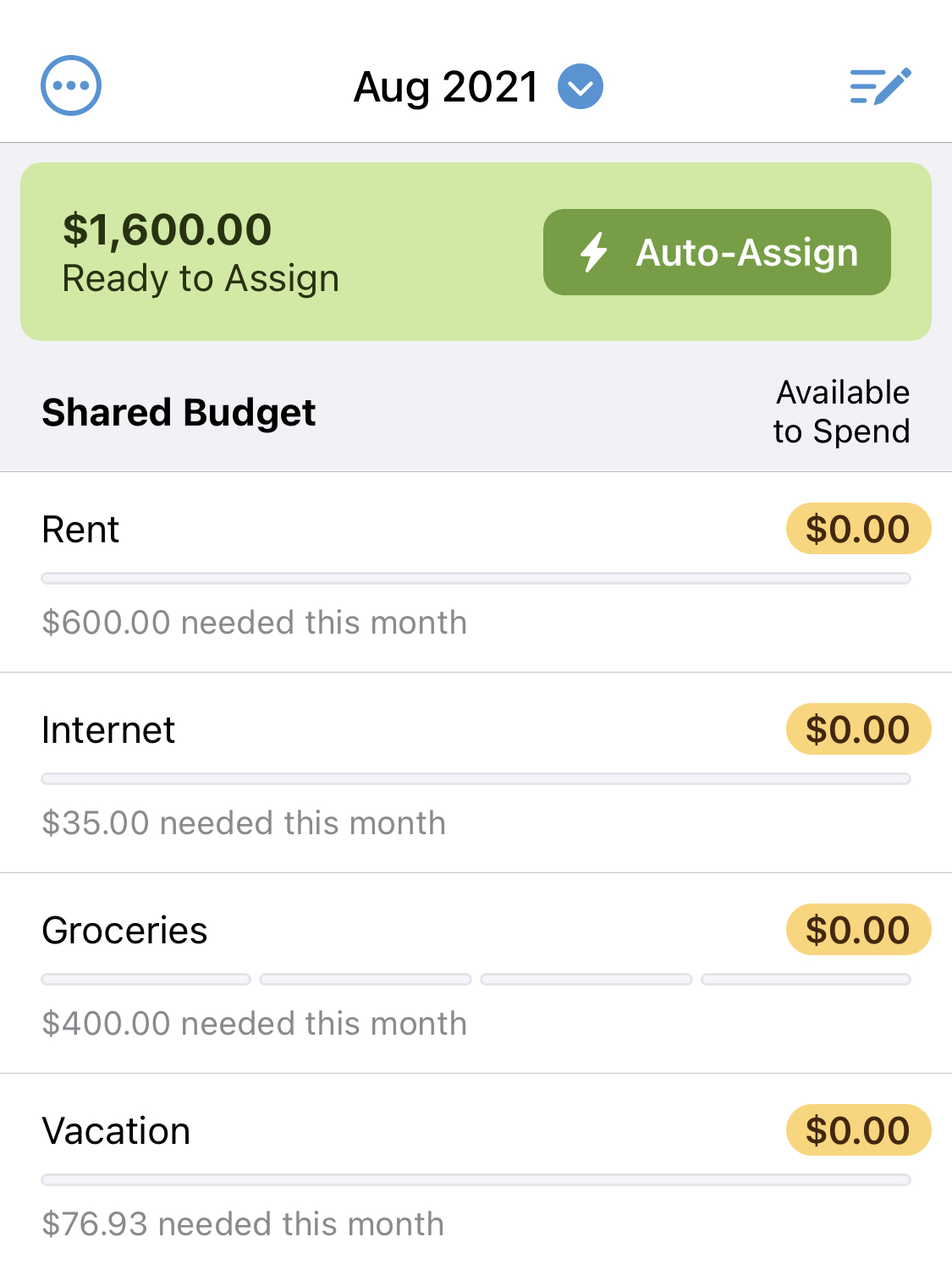

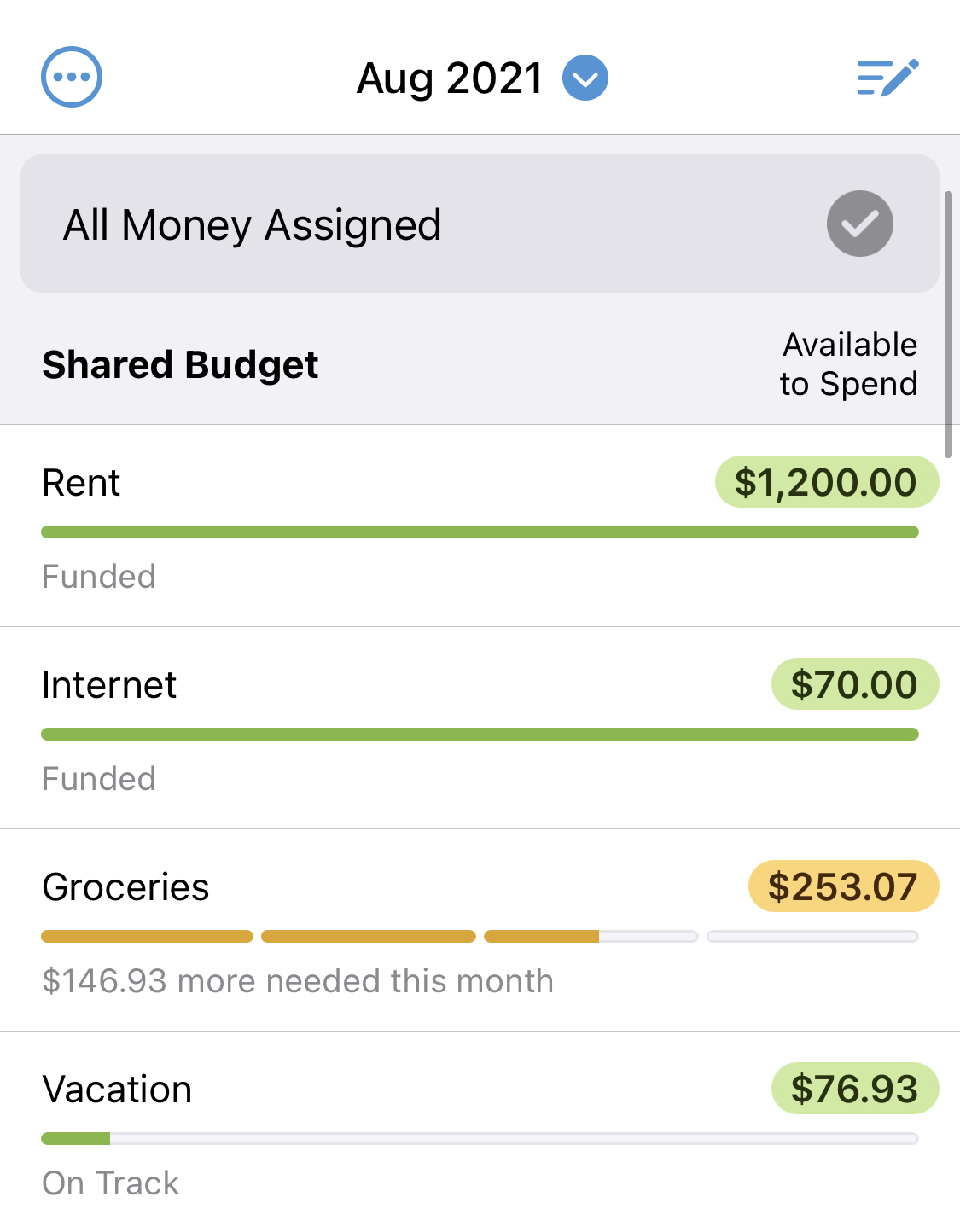

You can see in their YNAB budget below, they’ve each contributed $800 for a total of $1600 to be assigned in their shared budget.

3. Budget Household Expenses Together

Then, together, Jamie and Jordan use the household YNAB budget to assign jobs to the dollars in the household’s checking account. Those dollars cover shared bills and expenses, like the rent/mortgage, utilities, entertainment, an emergency fund, and shared food.

4. Make Decisions About Shared Goals in the Shared Budget

Jamie and Jordan set up categories in their shared budget for joint goals like vacations, holiday gifts, and semi-annual insurance premiums. Together, they work together to fund those.

Speaking of goals, Jamie and Jordan are wisely thinking ahead, and they’ve set up their household savings account to feed each of their Roth IRAs for saving for retirement, a tip their financial advisor recommended they set up when they asked about retirement planning.

The Benefits: Individual Control While Still a Team

This method may sound convoluted from a distance, but (still imaginary) Jamie and Jordan swear that it’s a cinch in practice for their personal finance setup. They also swear that the person who suggested it is extremely wise and probably very attractive. (Ahem.)

They like this method because:

- They are completely in control of their individual dollars—Jamie likes to experiment with cryptocurrency, and Jordan likes to travel. With this method, they can prioritize how they spend and save money on their own.

- Jamie is more of a saver, and Jordan is more of a spender. This system alleviates guilt about different money management styles and you can still track your spending (or saving).

- Jamie and Jordan are totally different when it comes to budgeting styles—Jordan’s always getting into details, while Jamie’s happy to let things go for a few weeks. For them, this method allows them to meet in the middle.

- They’re still a team! Even though they retain individual control, Jamie and Jordan still have a shared view of the money (and how their choices are affecting their future).

What You Could Miss

Now, I need to point out that all of the above can be accomplished (and simplified!) by using one budget and one joint-account—the benefits of which are not to be dismissed:

- Honesty (with each other and yourself!) is built-in

- Less complexity equals less risk that you’ll miss important details

- Greater focus on your true, shared priorities

But you do you! I’m just pointing stuff out over here.

What About Your Household?

In any relationship, there’s certainly an art in keeping the peace when it comes to money differences. We’re firm believers in the power of budgeting to bring relationships even closer. As funny as it sounds, managing money and expenses has a way of aligning what matters to both of you and putting you on the same page.

If you’re new to budgeting, we have a system that’s saved relationships, brought people together, and gotten couples working together to pay down debt, break the paycheck to paycheck cycle, and improve communication. Sign up for your free 34-day trial today.

The post Budgeting for Couples When You Don’t Share Accounts appeared first on You Need A Budget.

Via Finance http://www.rssmix.com/

No comments:

Post a Comment